傳統銀行儲蓄利率僅有 1-3%,而去中心化金融(DeFi)則以雙位數乃至三位數年化百分比收益(APY)為賣點,形成強烈對比。這一驚人差異吸引了數十億美元資本,參與者包含個人加密貨幣愛好者,也有尋求替代傳統投資管道的機構巨擘。

邁入 2025 年中,DeFi 生態圈核心問題是:這些驚人回報究竟象徵金融革命的永續新局,還是即將破滅的投機泡沫?這個問題並非紙上談兵——它影響著數以百萬計投資人、更廣泛的加密貨幣市場,甚至潛移默化整個金融系統。

DeFi 收益的可持續性位於科技創新、經濟理論、監管不確定性及金融行為演進的交會點。支持者認為,區塊鏈的效率提升與去除傳統中介,足以讓成熟市場持續維持高報酬。批評者則指出,目前收益水準反映的是難以延續的代幣經濟學、潛藏風險,以及暫時性的監管套利,而非真正的價值創造。

近期發展更讓此爭論升溫。貝萊德(BlackRock)專屬加密部門於 2025 年 3 月宣布擴大其 DeFi 業務,顯示機構投資興趣日增。與此同時,2025 年 1 月,VaultTech 等高收益協議倒閉,該協議曾承諾 35% 可持續 APY,卻導致投資人損失超過 2.5 億美元,進一步強化質疑者的憂慮。

本文將綜合分析正反意見,深入解析其運作機制、風險、歷史趨勢與新興創新,以洞悉 DeFi 高收益究竟是新金融典範,還是難以為繼的一時現象。

收益農場運作機制:DeFi 如何產生收益

DeFi 收益的基礎架構

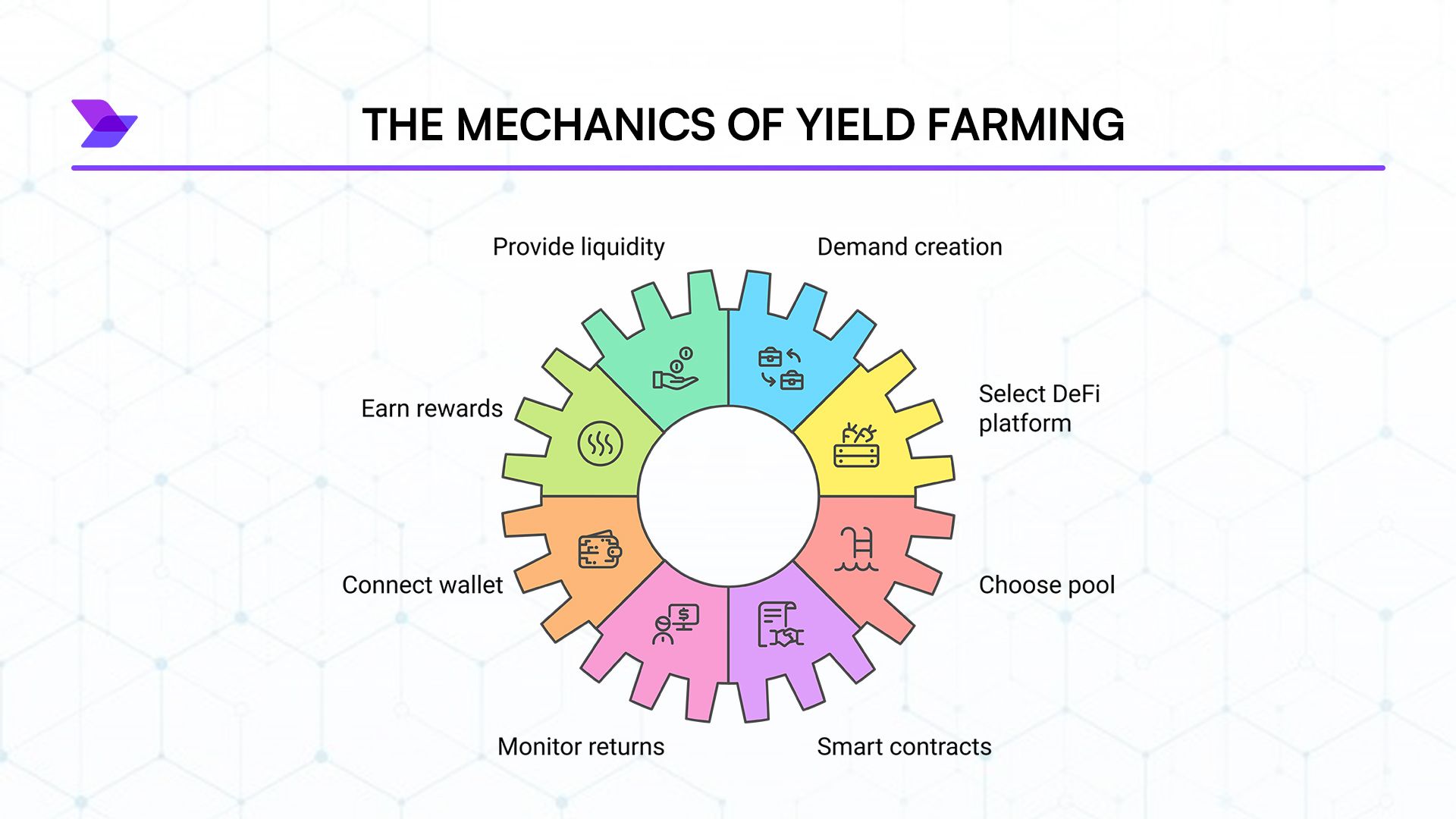

收益農場是 DeFi 價值主張的核心,透過機制讓用戶將自身數位資產注入去中心化協議,被動賺取收益。其本質為將加密貨幣存入流動性池(智能合約管理的資金池),為各種金融服務提供動力。這些池子支撐 DeFi 重要操作,如去中心化交易所(DEX)上的代幣兌換、信貸平台放貸或作為合成資產的抵押品。

用戶先將數位錢包連接到 DeFi 協議,並經由智能合約存入代幣。與傳統金融繁瑣的手續、身分驗證與營業時間不同,DeFi 交易全天候即時執行,門檻極低。例如,收益農夫可存入等值 1 萬美元的 ETH 與 USDC 到 Uniswap 的流動性池,為其他用戶提供代幣兌換所需流動性。

作為提供流動性的回饋,參與者可獲得多重收益:其一,通常可分潤協議產生的手續費——如 Uniswap 每筆交易抽取 0.3% 費用,按流動池份額分配給提供者。其二,許多協議會發放原生治理代幣作為額外激勵。

這種同時結合手續費與代幣獎勵的雙重獎勵架構,使 DeFi 出現吸睛的高收益,吸引數百萬用戶湧入。不過,欲判斷這些報酬能否持續,必須分開檢視各成分,因它們的運作邏輯本質不同。

常見收益農場策略類型

DeFi 生態自問世以來快速演進,衍生各式收益農場策略,滿足不同風險偏好、技術能力與資本規模所需。根據 CoinDesk 最新分析,主要策略如下:

流動性挖礦

流動性挖礦可說是最直接的收益農場策略。用戶將等值兩種代幣存入像 Uniswap、SushiSwap、PancakeSwap 等 DEX 的資金池。例如農夫存入 5,000 美元 ETH 及 5,000 美元 USDC 到 ETH/USDC 池,換得代表其股份的 LP(流動性提供者)代幣及手續費分潤,還常可獲得平台原生代幣獎勵。

流動性挖礦 APY 落差極大,成熟藍籌配對約 5%,新專案為吸納流動性則高達千分比。不過,高收益常伴隨更高風險,包括無常損失與低品質代幣曝險等。

借貸平台

借貸是另一基本的收益農場策略,用戶將資產存入像 Aave、Compound 或新興平台,賺取借款人利息。這些平台全由智能合約運作,無中央管控,運作機制類似銀行。

放貸收益由演算法根據供需自動調整——當借貸需求強勁,利率自然提升。多數平台又會發放額外代幣,提高綜合收益。比起流動性挖礦,借貸提供較穩健卻略低的報酬,適合風險趨避型用戶。

質押機制

質押的概念在 DeFi 中大幅擴展,早已超越「協助 PoS 區塊鏈安全」的基本功能,現今包括:

- 協議質押:鎖倉代幣參與治理並賺取獎勵

- 流動性質押:像 Lido 這類協議中存入 ETH 換取 stETH 等流動性質押代幣,可於多處再利用產生收益

- LP 代幣質押:將流動性挖礦獲得的 LP 代幣進行質押,賺取額外獎勵

流動性質押衍生品帶來強大可組合性,資產能同時多處賺取收益,此特性已成 2025 年 DeFi 關鍵。例如 Pendle Finance 創新品種化收益(yield tokenization),將資產本體與未來收益拆分交易與優化。

進階收益策略:發揮可組合性

DeFi 最具革命性的特質,是協議間高度可組合——可無縫串接創造越來越複雜的金融產品,即所謂「貨幣積木」。這造就傳統金融無法實現的進階收益策略。

收益聚合器

Yearn Finance 等平台開發智慧金庫,自動分配資金到多個收益來源,以優化報酬、降低風險與手續費。這些聚合器實作複雜策略,包括:

- 根據不同收益來源績效自動再平衡

- 把存入資產借出以杠桿放大利潤

- 自動複利最大化 APY

- 執行閃電貸在各協議間套利

截至 2025 年 2 月,Yearn 金庫管理資產總額已逾 110 億美元,其主打穩定幣策略即使在熊市,依然穩定提供 15–20% APY。該協議說明,自動化與優化可憑效率而非大量釋放代幣,創造可持續收益。

衍生品與選擇權策略

DeFi 日益成熟,促成複雜衍生品與選擇權協議誕生,創造全新收益來源。Opyn、Ribbon Finance 等平台提供架構化產品,透過選擇權策略產生收益:

- 複合買權 Vault:透過出售持有資產的買權收取權利金

- 賣出賣權 Vault:提供保證金賣出賣權

- 波動套利:利用不同到期日間的價格效率套利

這類策略更貼近傳統金融工程,相較於早期 DeFi 單純農場,有潛力創造真正由市場活動產生、較為可持續的收益。

高報酬永續性的論點

區塊鏈的效率優勢

若要判斷 DeFi 高收益是否具有永續性,首先必須分析區塊鏈與智能合約較傳統金融基礎建設所具有的技術優勢。這些潛力甚至能讓市場成熟後依然維持較高報酬。

區塊鏈技術核心在於前所未有的規模與效率下,實現無信任協作。傳統金融系統多重冗餘並需跨機構對帳。舉例而言,證券交易執行時,需多方分別維護帳本並反覆核對——這一流程可能需時數日且涉及 substantial manual work despite decades of digitization efforts.

儘管數十年來致力於數位化,許多流程仍需要大量人工處理。

Blockchain's shared ledger eliminates this redundancy by creating a single source of truth that all participants can verify independently. This architectural shift dramatically reduces overhead costs. Major banks typically spend 5-10% of their operating budgets on reconciliation processes that blockchain renders largely unnecessary, according to McKinsey's 2024 Banking Technology Report.

區塊鏈的共享帳本消除了這種重複作業,建立了一個所有參與方都能獨立驗證的單一真實資料來源。這種架構上的轉變大幅降低了間接成本。根據麥肯錫 2024 年銀行科技報告,大型銀行通常將營運預算的 5-10% 用於「對帳」流程,而區塊鏈可以讓這些流程基本變得不再需要。

Smart contracts further amplify these efficiency advantages by automating complex financial logic. The traditional loan issuance process typically involves application processing, credit checks, manual underwriting, legal documentation, and servicing - all performed by various professionals whose compensation ultimately comes from the spread between deposit and lending rates. In contrast, lending protocols like Aave or Compound automate this entire workflow through smart contracts that execute instantly at minimal cost.

智能合約進一步放大了這些效率優勢,可以自動處理複雜的金融邏輯。傳統放款流程通常包含申請處理、徵信審查、人工審核、法律文件和後續服務,這些都需要不同的專業人士來執行,其報酬最終來自存放利差。相較之下,Aave 或 Compound 這類借貸協議能透過智能合約將整個流程自動化,即時執行且成本極低。

This fundamental efficiency advantage creates a technological "yield premium" that could persist indefinitely, similar to how internet businesses maintain structural advantages over brick-and-mortar counterparts. The magnitude of this premium remains debatable, but analyses from Messari Research suggest it could sustainably add 2-5% to returns across various financial activities.

這種基本的效率優勢產生了一種「科技收益溢價」,可能會長期持續,就如同網路公司相較於傳統實體產業保有結構性競爭力一樣。這個溢價的幅度仍有爭議,但Messari Research 的分析顯示,這可能為多種金融活動帶來可持續的 2-5% 額外報酬。

Disintermediation: Cutting Out the Middlemen

去中介化:消除中間人

Beyond pure technical efficiency, DeFi creates substantial value through aggressive disintermediation - removing layers of middlemen who extract fees throughout the traditional financial value chain. This disintermediation represents perhaps the strongest case for sustainable higher yields in decentralized finance.

除了純粹的技術效率外,DeFi 透過強力的去中介化創造了巨大價值——徹底移除傳統金融價值鏈中各種收取費用的中間層。這項去中介化,也許是去中心化金融能夠實現永續高收益的最有力論據。

The traditional financial system relies on an extensive network of intermediaries, each extracting value:

傳統金融系統仰賴龐大的中介網絡,每一環都在抽取價值:

- Retail banks charge account fees and profit from deposit-lending spreads

- 投資銀行收取承銷費、交易佣金及顧問費

- 資產管理公司每年收取0.5%-2%的管理費

- 經紀商靠交易差價與執行費用獲利

- 結算所收取清算與託管服務費

DeFi systematically eliminates most of these intermediaries through direct peer-to-peer transactions governed by smart contracts. When a user provides liquidity to a DEX or lends through a DeFi protocol, they interact directly with counterparties without intermediaries extracting value between them.

DeFi 以智能合約主導的點對點交易,系統性地淘汰了上述多數中介。用戶將資金提供給 DEX 或借貸協議時,是直接和對手方互動,中間不再有層層抽取價值的中介者。

This streamlined value chain allows substantially more economic value to flow directly to capital providers rather than intermediaries. For instance, when traders swap tokens on a DEX, approximately 70-90% of trading fees go directly to liquidity providers, compared to perhaps 20-30% in traditional market-making arrangements.

如此精簡的價值鏈,能讓更多經濟價值直接流向資本提供者,而不是中間人。例如,交易者在 DEX 換幣時,約有 70-90% 的手續費直接分給流動性提供者,而傳統做市商模式通常只有 20-30%。

A December 2024 analysis by WinterTrust compared fee structures across traditional and decentralized finance, finding that DeFi protocols operate with approximately 70-80% lower overhead costs. This efficiency allows protocols to simultaneously offer higher yields to capital providers and lower fees to users - a win-win that suggests the disintermediation advantage could sustain higher returns permanently.

2024 年 12 月 WinterTrust 的分析顯示,DeFi 協議比傳統金融系統的營運成本低約 70-80%。這種效率讓協議能同時給資本提供者更高回報、給用戶更低費用——雙贏,這也意味去中介化優勢可能使高報酬成為常態。

Innovative Tokenomics

創新代幣經濟學

The innovative tokenomic models pioneered within DeFi represent another potential source of sustainable high yields. While critics often dismiss token incentives as merely inflationary, closer examination reveals sophisticated economic designs that can potentially sustain attractive yields through genuine value creation and distribution.

DeFi 所首創的創新代幣經濟模式,構成另一個潛在的永續高收益來源。雖然批評者常將代幣激勵視為單純的通膨工具,實際深入分析會發現,其背後有著成熟的經濟設計,能夠透過真正的價值創造與分配,維持具吸引力的報酬。

Governance tokens - which confer voting rights over protocol parameters and development - constitute a fundamental innovation in financial system design. Unlike traditional financial institutions where governance rights concentrate among shareholders (typically excluding customers), DeFi protocols often distribute governance power broadly to users, aligning incentives throughout the ecosystem.

治理代幣—賦予協議參與者針對參數和開發方向的投票權—是金融系統設計上的關鍵創新。有別於傳統金融治理權集中於股東(多半不含用戶),DeFi 協議往往把治理權廣泛分配給用戶,使整個生態系充分對齊激勵。

The most advanced protocols have evolved beyond simple inflationary tokenomics to implement sustainable value capture mechanisms:

最先進的協議已經超越了單純通膨獎勵,導入永續價值擷取機制:

- 手續費分潤模式:例如 Curve Finance 及 Sushi,把部分交易手續費分配給代幣質押者

- 協議自有流動性:由 Olympus DAO 首創,眾多新專案跟進,允許協議自行管理庫存資產獲取永續收益

- 實體資產整合:如 Centrifuge,將 DeFi 與實體資產(像不動產及貿易金融)串連,讓產生收益有實質經濟活動背書

These innovative models represent a fundamental evolution beyond the simple "print tokens for yield" approach that dominated early DeFi. By aligning token economics with genuine value creation and capture, these protocols create potentially sustainable yield sources that don't rely solely on new capital inflows.

這些創新的經濟模式,已大幅超越早期「印代幣發獎勵」的粗糙做法。當代幣經濟學和實際價值創造、擷取機制結合,DeFi 協議便可能產生不必單靠新資金流入的永續收益來源。

The Capital Efficiency Revolution

資本效率革命

The ongoing evolution of capital efficiency within DeFi represents perhaps the most promising technological development for sustainable yields. Traditional finance operates with significant capital inefficiencies - banks maintain substantial reserves, assets remain siloed across different services, and capital moves slowly between opportunities.

DeFi 在資本效率上的持續創新,是永續高收益最有潛力的科技革命。傳統金融存在嚴重資本低效—銀行需要大量準備金、資產分散在不同服務、資金轉移緩慢等問題。

DeFi's composability and programmability have sparked a revolution in capital efficiency through innovations like:

DeFi 的可組合性與可程式化特性,帶來下列提升資本效率的創新:

- 集中流動性:Uniswap v3、Ambient 等協議讓流動性供應者可將資金聚集於特定價格區間,放大實際報酬

- 迴圈借貸:平台允許用戶先存入資產再借出資產,再將借出資產回存,多次循環以倍增風險及收益

- 彈性供給代幣:如 OHM 與 AMPL,自動調節代幣供給,創造新型收益模式

- 閃電貸:單一鏈上交易區塊內的無抵押極短貸款,能高效執行套利與收益最佳化

These capital efficiency innovations allow the same underlying assets to generate multiple layers of yield simultaneously - a fundamental breakthrough compared to traditional finance. A March 2025 paper from Stanford's Blockchain Research Center calculated that DeFi's capital efficiency innovations could theoretically support sustainable yields 3-7% higher than traditional finance while maintaining equivalent risk profiles.

這些資本效率創新允許底層資產同時產生多重收益層,相較傳統金融是根本性的突破。斯坦福區塊鏈研究中心 2025 年 3 月論文計算指出,DeFi 的資本效率創新理論上可支持比傳統金融高 3-7% 的永續收益,且維持風險水準不變。

Global Access and Market Inefficiencies

全球開放與市場效率差異

DeFi's permissionless nature creates another potential source of sustainable yield advantage: global accessibility. Traditional finance operates within national boundaries, creating significant market inefficiencies and yield discrepancies across regions. DeFi transcends these boundaries, potentially enabling persistently higher yields by tapping into global market opportunities.

DeFi 的無需許可(permissionless)特性,帶來另一種永續收益優勢:全球性的無障礙參與。傳統金融受限於國界,導致區域間存在明顯市場效率落差與利差。DeFi 則打破這些限制,有機會持續從全球市場套利,帶來更高收益。

For instance, while U.S. Treasury yields might offer 2-3%, emerging market government bonds might yield 8-12% for similar risk profiles after accounting for currency fluctuations. Traditional finance makes accessing these opportunities difficult for average investors due to regulatory barriers, while DeFi platforms can integrate global opportunities seamlessly.

舉例來說,美國國債收益率可能僅有 2-3%,但若算入匯率風險,新興市場國債卻常有 8-12% 可比風險的收益。傳統金融因法規與隔閡,讓一般投資人難以涉足這些機會,而 DeFi 平台則可無縫整合全球機會。

This global arbitrage opportunity extends beyond government bonds. DeFi protocols increasingly connect with real-world assets across jurisdictions, accessing yield opportunities previously available only to sophisticated institutional investors. Platforms like Goldfinch and TrueFi have pioneered uncollateralized lending to businesses in emerging markets, generating sustainable 15-20% yields backed by real economic activity rather than token emissions.

這種全球套利機會不限於公債。DeFi 協議正快速連結各地實體資產,打開過去只有專業機構可碰觸的投資標的。例如,Goldfinch 和 TrueFi 創新地向新興市場企業提供無抵押貸款,產生 15-20% 的永續收益,這些收益是由實體經濟活動支撐而非單純賦予代幣。

As DeFi continues bridging global financial gaps, this geographic arbitrage could sustain yield premiums for years or decades until global financial markets achieve perfect efficiency - a distant prospect given persistent regulatory and infrastructure barriers.

隨著 DeFi 持續彌合全球金融鴻溝,這類地理性套利效應可能維持高報酬數年甚至數十年,除非全球金融系統真能完全走向完美效率,而這在當前的法規與基礎建設現狀下仍遙不可及。

The Case Against High Returns: Systemic Risks

反對高報酬的理由:系統性風險

Inflated Tokenomics

通膨型代幣經濟的風險

While proponents highlight DeFi's innovative tokenomic designs, critics argue that many protocols rely on fundamentally unsustainable emission schedules that mathematically cannot maintain their high yields over time. A rigorous analysis of these token models reveals significant concerns about long-term sustainability.

儘管支持者強調 DeFi 創新代幣模組,批評者則指出許多協議其實仰賴極不永續的發幣機制,從數學上就無法長期維持高年化。對這些發幣模型的嚴謹分析發現,長期可持續性有嚴重疑慮。

Many DeFi protocols distribute governance tokens as yield incentives according to predetermined emission schedules. These schedules typically follow patterns like constant emission (a fixed number of tokens distributed daily) or gradual reduction (emissions decrease by a small percentage each period). Without corresponding growth in demand or token utilities, this supply expansion mathematically leads to price depreciation.

許多 DeFi 協議採用預設的發幣計劃,將治理代幣作為收益獎勵分發。這些發放設計通常是固定量每日發幣,或逐步遞減,但如果沒有需求同步成長或代幣用途增加,供給膨脹最終會導致價格貶值是數學必然。

Token emissions inherently dilute existing holders unless the protocol generates sufficient new value to offset this expansion. This dilution creates a zero-sum dynamic where early farmers benefit at the expense of later participants - a mathematical reality often obscured by bull market token appreciation. The most concerning tokenomic models exhibit characteristics that mathematicians and economists identify as structurally similar to Ponzi schemes, where returns for existing participants depend primarily on capital from new entrants rather than sustainable value creation.

幣量發行如果不能靠協議持續產生新價值來對沖,就勢必稀釋持有人資產。這種稀釋造成的結果就是「早挖得利、晚來受損」,本質上是零和博弈,只是在牛市幣價上漲時容易被忽略。有些最值得警惕的代幣模型,甚至被數學家與經濟學家判定與龐氏詐騙在結構上極為接近——現有參與者收益主要來源是後來資金,而非自體創造實質新價值。

A comprehensive analysis by CryptoResearch examined emission schedules of 50 leading DeFi protocols, finding

[下文未完,待續。]that 36% were mathematically certain to experience significant yield compression regardless of protocol adoption or market conditions. The research identified several concerning patterns:

有36%的協議,即使不考慮協議採用狀況或市場環境,數學上也必然會經歷顯著的收益壓縮。研究指出了幾個令人擔憂的模式:

-

Emissions exceeding revenue: Protocols distributing token rewards valued at 3-10x their actual fee revenue

-

Death spiral vulnerability: Tokenomics where declining prices trigger increased emissions, further depressing prices

-

Governance concentration: Projects where insiders control sufficient voting power to perpetuate unsustainable emissions for personal benefit

-

代幣激勵遠超實際收入:協議發放的代幣獎勵價值為實際手續費收入的3-10倍

-

死亡螺旋風險:當代幣價格下跌時激發更高發行,進一步壓低價格的代幣經濟設計

-

治理權力過度集中:內部人士掌握足夠投票權,可為個人利益無限延續不可持續的獎勵發放

These fundamentally unsustainable tokenomic designs have already led to several high-profile protocol collapses, including UmaMi Finance in June 2024 and the MetaVault crisis in November 2024. Both platforms promised "sustainable" high yields that mathematically could not continue beyond their initial growth phases.

這些根本無法長期維持的代幣經濟設計,已導致多起知名協議崩潰事件,例如2024年6月的UmaMi Finance,以及2024年11月的MetaVault危機。這兩個平台都曾承諾「可持續」的高收益,但從數學角度來看,這些收益根本不可能超過初期發展階段。

Impermanent Loss: The Hidden Yield Killer

無常損失:隱形的收益殺手

While DeFi marketing materials emphasize attractive APYs, they often minimize or omit discussion of impermanent loss (IL) - a unique risk that can significantly erode or even eliminate returns for liquidity providers. Understanding this phenomenon is crucial for assessing the true sustainability of DeFi yields.

雖然DeFi的行銷內容強調誘人的年化收益率(APY),但往往淡化或忽略「無常損失」(IL)這一重大風險。這種獨特的風險可能嚴重侵蝕,甚至直接消滅流動性提供者的實際回報。理解這一現象,對於評估DeFi收益的真正可持續性至關重要。

Impermanent loss occurs when the price ratio between assets in a liquidity pool changes from when liquidity was provided. Mathematically, it represents the difference between holding assets passively versus providing them to an automated market maker (AMM). For volatile asset pairs, this loss can be substantial:

無常損失發生於流動性池中,兩種資產的價格比與剛提供流動性時相比有所變動。從數學上來說,它代表了被動持有資產與將資產提供給自動化做市商(AMM)之間的收益差額。對於波動大的資產組合,損失可能非常可觀:

-

25% price change in one asset: ~0.6% loss

-

50% price change in one asset: ~2.0% loss

-

100% price change in one asset: ~5.7% loss

-

200% price change in one asset: ~13.4% loss

-

一種資產價格變動25%:約0.6%損失

-

一種資產價格變動50%:約2.0%損失

-

一種資產價格變動100%:約5.7%損失

-

一種資產價格變動200%:約13.4%損失

These losses directly reduce the effective yield for liquidity providers. For instance, a pool advertising 20% APY might deliver only 7-8% actual returns after accounting for IL in a volatile market. In extreme cases, impermanent loss can exceed base yields entirely, resulting in net losses compared to simply holding the assets.

這些損失將直接削減流動性提供者的實際收益率。例如,一個標榜20% APY的池子,在波動劇烈的市場中,扣除無常損失後實際僅能獲得約7-8%的回報。在極端情況下,無常損失甚至會吃掉全部基礎收益,導致持幣者相比單純持有資產還要虧損。

Research from the Imperial College London examined historical performance across major AMMs, finding that impermanent loss averaged 2-15% annually for typical liquidity providers, with some volatile pairs experiencing losses exceeding 50%. This hidden cost fundamentally undermines the sustainability narrative of many high-yield liquidity mining opportunities.

[帝國理工學院的研究] 檢視了主要AMM的歷史表現,發現一般流動性提供者每年平均遭受2-15%的無常損失,一些波動極大的資產對甚至損失超過50%。這種隱形成本根本動搖了許多「高收益」流動性挖礦機會的可持續性敘事。

The challenge of impermanent loss represents a structural inefficiency in current DeFi models that may prevent sustained high yields from liquidity provision. While innovations like concentrated liquidity and active management strategies attempt to mitigate these effects, they introduce additional complexity and costs that may ultimately limit sustainable yield potential.

無常損失的挑戰,揭示出現有DeFi模型的結構性低效,這或許將使流動性挖礦無法長期維持高收益。雖然集中流動性等創新和主動管理策略有助於減輕這一問題,但這些方法同時帶來更高的複雜度與成本,最終仍會對可持續收益潛力造成限制。

Smart Contract Vulnerabilities

智能合約漏洞

Beyond tokenomic and market risks, DeFi yields face a more existential threat: the security vulnerabilities inherent in the smart contracts that form the foundation of the entire ecosystem. These vulnerabilities challenge the notion of sustainable yields by introducing catastrophic tail risks not typically present in traditional financial instruments.

除了代幣經濟及市場風險外,DeFi收益還必須面對更根本的威脅:驅動整個生態系的智能合約存在的安全漏洞。這些漏洞帶來極端的尾部風險,這種信用毀滅性的風險在傳統金融工具中極為罕見,從根本上質疑所謂的可持續收益。

The DeFi landscape has been plagued by persistent security breaches that have resulted in billions of dollars in losses. Even in 2025, after years of security improvements, significant exploits continue to occur with alarming regularity. Analysis of major DeFi hacks reveals common attack vectors that persist despite awareness:

DeFi生態始終遭受安全事故困擾,累積損失金額達數十億美元。即使到2025年經過多年安全強化,重大的攻擊事件仍屢見不鮮。對多起重大DeFi駭客事件的分析顯示,以下攻擊手法即使廣為人知,仍反覆出現:

-

Flash loan attacks: Exploiting temporary market manipulations using uncollateralized loans

-

Oracle manipulations: Tampering with price feeds to trigger advantageous liquidations

-

Reentrancy vulnerabilities: Exploiting function call sequences to withdraw funds multiple times

-

Access control failures: Targeting inadequate permission systems

-

Logic errors: Exploiting flawed business logic in complex financial mechanisms

-

閃電貸攻擊:利用無抵押貸款進行臨時市場操縱

-

預言機操縱:竄改價格來源,觸發有利的清算行為

-

重入漏洞:利用合約呼叫流程不當,多次提取資金

-

權限控管失效:針對許可機制不完善的系統

-

業務邏輯錯誤:利用複雜金融機制中的錯誤邏輯

The persistence of these vulnerabilities raises fundamental questions about yield sustainability. Any yield calculation must account for the non-zero probability of complete principal loss through smart contract failure - a risk that compounds over time and exposure to multiple protocols.

這些安全風險長期存在,使得收益可持續性存疑。所有的預期收益計算中,事實上都必須納入「因合約失效而本金歸零」的非零概率,這種風險隨著時間和協議覆蓋範圍增加而不斷累積。

The DeFi SAFU Report 2025 examined five years of security incidents across the ecosystem, finding that despite improvements in security practices, the annualized loss rate from hacks and exploits still averaged 4.2% of total value locked (TVL). This effectively creates an ecosystem-wide insurance premium that should theoretically reduce sustainable yields by a corresponding amount.

[DeFi SAFU報告 2025] 分析了整個生態過去五年的安全事件,發現即使安全措施有所提升,由駭客攻擊和漏洞造成的年化損失率,仍然平均達TVL的4.2%。這等於賦予了全行業一筆隱性的保險費,理論上應折抵掉等值的可持續年化收益。

This security tax represents a persistent cost that may limit the sustainable yield advantage of DeFi over traditional finance. While individual protocols might demonstrate excellent security records, users typically diversify across multiple platforms, increasing their cumulative exposure to these tail risks.

這項安全「稅收」構成持續成本,或會限制DeFi相對傳統金融的結構性收益優勢。即便某些協議安全紀錄優異,使用者一般會將資金分散於多平台,這反而擴大了整體風險敞口。

Regulatory Uncertainty

監管不確定性

While technical and economic factors significantly impact yield sustainability, regulatory considerations may ultimately prove even more determinative. The evolving regulatory landscape poses existential challenges to many DeFi yield mechanisms that have largely operated in a gray area of compliance.

即使技術與經濟層面對收益可持續性已有重大影響,監管因素最終仍可能起決定性作用。隨著監管環境變動,許多DeFi收益機制面臨根本性的生存壓力,因它們多處於合規灰色地帶。

As of 2025, the regulatory environment for DeFi remains fragmented globally but has significantly clarified compared to earlier years. Key developments include:

截至2025年,全球DeFi監管雖仍分散,較早期已有顯著明朗化。關鍵進展包括:

-

Securities classification frameworks: The SEC has intensified efforts to classify many DeFi tokens as securities, with landmark cases against major protocols

-

KYC/AML requirements: Several jurisdictions now mandate identity verification for DeFi participants, challenging the anonymous nature of many yield mechanisms

-

Stablecoin regulation: The implementation of the Global Stablecoin Framework has imposed reserve requirements and transparency standards

-

Tax enforcement: Advanced blockchain analytics have enabled more aggressive tax authority monitoring of DeFi activities

-

證券歸類框架:美國SEC大力推動將許多DeFi代幣歸類為證券,並針對主要協議展開標竿訴訟

-

KYC/AML規定:多個司法轄區已強制要求DeFi參與者實名認證,衝擊了許多收益機制的匿名屬性

-

穩定幣監管:全球穩定幣框架上路,要求準備金以及資訊透明

-

稅務強化:先進區塊鏈分析技術,使稅務機關能更積極追蹤DeFi活動

These regulatory developments create significant compliance challenges for protocols built on permissionless, pseudonymous foundations. Many high-yield strategies explicitly rely on regulatory arbitrage - the ability to operate without the compliance costs and capital requirements imposed on traditional financial entities. As regulatory pressure increases, some portion of DeFi's yield advantage may derive from temporary regulatory arbitrage rather than sustainable innovation.

這些監管新政,對建立於無需許可、偽匿名基礎上的協議構成重大合規挑戰。許多高收益策略明顯倚賴「監管套利」——即繞過傳統金融機構必須負擔的合規成本與資本要求。隨著監管壓力加大,外界逐漸質疑DeFi的收益優勢,到底來源於暫時的監管套利,還是真正的可持續創新。

The Compliance Cost Index published by blockchain analytics firm Elliptic estimates that full regulatory compliance would add operating costs equivalent to 2-5% of TVL for most DeFi protocols. This suggests that some portion of current yield advantages may erode as regulatory clarity forces protocols to implement more comprehensive compliance measures.

區塊鏈分析公司Elliptic發布的 [合規成本指數] 估算,若DeFi協議完全遵循監管,相關營運成本將占TVL的2-5%。這意味著,隨著監管明確化並強制落實合規,現有部分收益優勢勢必消耗殆盡。

Capital Concentration and Competitive Dynamics

資本集中與競爭動態

The DeFi ecosystem has exhibited strong winner-take-all tendencies that may ultimately compress yields through capital concentration and competitive dynamics. As markets mature, capital tends to flow toward protocols with the strongest security records, most efficient mechanisms, and deepest liquidity - a pattern that naturally compresses yields through competition.

DeFi生態本身呈現強烈的贏者通吃特性,隨著資本集中和競爭加劇,最終將壓縮整體收益率。市場逐步成熟後,資金自然流向安全性最高、機制效率最佳、流動性最深的協議,這種格局促使收益透過激烈競爭被壓平。

This competitive dynamic has already manifested in several segments of the DeFi ecosystem

這種競爭態勢已經在DeFi多個領域展現:

-

Stablecoin yields: Maximum yields have declined from 20-30% in 2021 to 8-12% in 2025 as capital concentration has increased efficiency

-

Blue-chip lending: Yields on established assets like ETH and BTC have compressed from 3-10% to 1-4% as competition intensified

-

Major DEXs: Liquidity provider returns have standardized around 5-10% annually for popular pairs, down from 20-50% in earlier years

-

穩定幣收益:頂峰年化收益自2021年的20-30%,壓縮至2025年的8-12%,效率因資本集中而提升

-

藍籌借貸:像ETH、BTC等主流資產的借貸年化收益,已由3-10%降至1-4%

-

主流去中心化交易所:熱門交易組合的流動性提供者年化報酬穩定在5-10%,而早年曾高達20-50%

The inevitable capital concentration process threatens the sustainability of outlier high yields across the ecosystem. As protocols compete for liquidity and users, economic theory suggests they will ultimately converge toward an efficient frontier where returns balance risk factors appropriately.

這種資本不可逆集中過程,將使全生態系無法維持異常高收益。隨著協議間爭奪流動性和用戶,經濟理論指出,最終利潤會趨於風險報酬均衡的有效前緣。

Research from the University of Basel examined yield compression across DeFi protocols from 2020-2024, finding that yields tended to converge toward equilibrium points approximately 3-5% above comparable traditional finance alternatives once protocols reached maturity. This suggests that while DeFi may maintain a structural yield advantage, the triple-digit returns that attracted early adopters may prove fundamentally unsustainable in the long term.

[巴塞爾大學的研究] 分析2020-2024年間DeFi協議的收益壓縮趨勢,發現協議成熟後收益普遍收斂於比傳統金融產品高3-5%的均衡點。這顯示,DeFi或能保持一定結構性利差,但那些曾吸引早期用戶的三位數報酬,長期來看基本不可能持續。

Historical Data and Yield Trends

歷史數據與收益趨勢

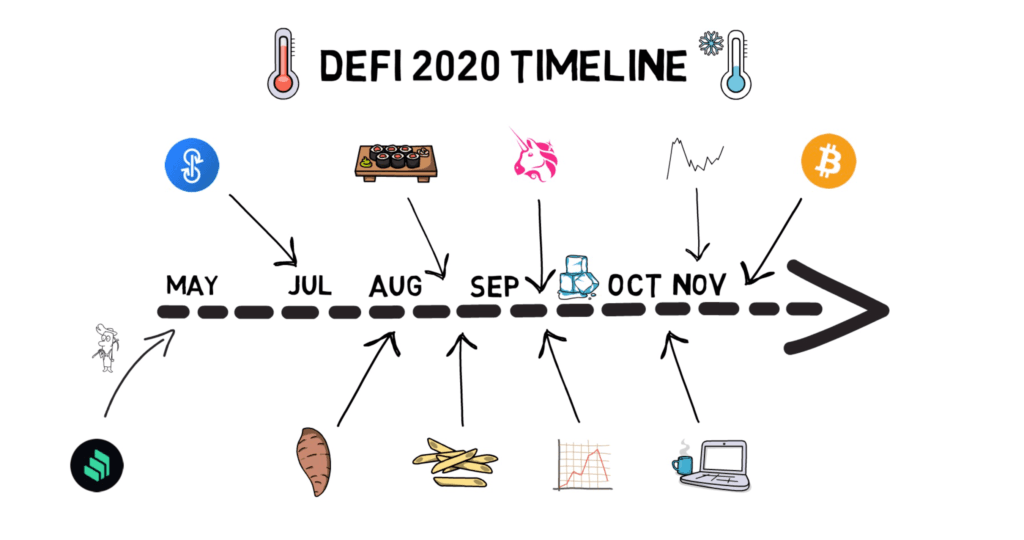

The DeFi Summer of 2020 and Beyond

2020年DeFi熱潮及其後續

The period known as "DeFi Summer" in 2020 represents a critical reference point for analyzing yield sustainability. This formative period saw explosive growth in DeFi protocols and introduced yield farming to mainstream crypto consciousness.

「DeFi夏季」的2020年,已成為分析收益可持續性的重要參考節點。這段時期見證了DeFi協議的爆發性成長,也讓「收益農耕」(Yield Farming)正式進入主流加密貨幣圈視野。

The catalyst for DeFi Summer came in June 2020 when Compound launched its COMP governance token and began distributing it to users based on protocol interaction. This innovation triggered a domino effect as users discovered they could earn triple-digit APYs through increasingly complex strategies involving lending, borrowing, and providing liquidity.

這股熱潮的導火線,是Compound在2020年6月推出COMP治理代幣,並根據用戶與協議互動情況發放代幣。這項創舉引發多米諾骨牌效應,當時用戶意識到結合借貸、放貸、流動性等複雜策略後,能拿到高達三位數的年化收益。

Key metrics from this period illustrate its exceptional nature:

這段時期的核心數據突顯其非凡之處:

-

TVL Growth: DeFi's total value locked expanded from approximately $1 billion in May 2020 to over $15 billion by September 2020

-

Token Valuations: Governance tokens like YFI surged from zero to over $40,000 in months

-

Yield Levels: Common strategies regularly offered 100-1,000% APY

-

TVL增長:DeFi總鎖倉價值從2020年5月的約10億美元,激增到2020年9月的超過150億美元

-

代幣估值:如YFI等治理代幣,數月內由零暴漲至4萬美元以上

-

收益水準:常見策略動輒開出100-1000%的年化報酬

This period established the template for token-incentivized growth that has defined much of DeFi's evolution. However, it also demonstrated

這一時期建立了以代幣激勵推動增長的標準模式,並深刻影響了DeFi此後的發展方向。然而,這同時也展現了...how unsustainable many early yield models were - by late 2020, many of the initially eye-catching yields had already compressed significantly as capital flooded into farming opportunities.

(許多早期收益模型究竟有多不可持續?——到2020年底,許多一開始引人注目的高收益,隨著資本湧入挖礦機會,已經大幅收斂。)

Yield Compression and Market Cycles

One of the most significant patterns in DeFi's evolution has been the progressive compression of yields across most strategies. This compression provides important evidence regarding the equilibrium level of sustainable returns in a maturing market.

(DeFi 發展過程中最顯著的現象之一,就是各種策略下收益率的逐步壓縮。這種壓縮現象為成熟市場中可持續回報的均衡水準,提供了重要證據。)

During the 2020-2021 bull market, DeFi yields displayed several characteristic patterns:

(在2020-2021年牛市期間,DeFi 收益展現出數個典型特徵:)

- Correlation with token prices: Yields denominated in dollars increased as governance token values appreciated

(與代幣價格的關聯:以美元計價的收益,因治理型代幣價格上漲而增加) - Protocol proliferation: New platforms launched with aggressive incentives, creating yield spikes

(協議爆發:新平台推出激進激勵措施,帶來收益飆升) - Capital efficiency innovations: Protocols developed increasingly sophisticated strategies

(資本效率創新:協議設計愈加精巧的收益策略) - Leverage expansion: Users employed greater leverage to amplify yields

(槓桿擴大:用戶使用更高槓桿放大收益)

The subsequent 2022-2023 bear market provided a crucial stress test for DeFi yield sustainability. As token prices declined sharply, many yield sources collapsed or significantly compressed. In particular, the market downturn exposed the unsustainable nature of yields based primarily on token emissions.

(隨後的 2022-2023 年熊市,為 DeFi 收益的可持續性帶來關鍵壓力測試。代幣價格劇烈下跌時,許多收益來源或消失、或大幅萎縮。尤其是,那些主要依賴代幣發放的收益,在市場下行時暴露出其不可持續的本質。)

By 2024-2025, a clearer pattern has emerged: protocols generating yields from actual usage fees, liquidations, and financial activities showed relatively stable returns regardless of market conditions. In contrast, yields derived primarily from token emissions or speculative demand fluctuated dramatically with market sentiment. This pattern suggests a core yield advantage derived from genuine efficiency gains and disintermediation benefits, upon which cyclical components layer additional returns during expansionary periods.

(到了2024-2025年,更清晰的格局浮現:那些從實際使用費用、清算及金融業務產生收益的協議,不論市況如何,都維持著較為穩定的回報。相對地,主要靠代幣發放或投機需求產生的收益,則隨著市場情緒大起大落。這說明,真正的「核心收益」來自效率提升與去中介化帶來的優勢,而週期性因素則只是在擴張期額外疊加;擁有核心優勢的協議能更為可持續。)

DeFi Llama's Yield Index has tracked this evolution since 2021, showing that sustainable "core yields" across the ecosystem have stabilized in the 5-15% range for most major assets and strategies. This represents a significant compression from earlier periods but still maintains a substantial premium over traditional finance alternatives.

(DeFi Llama 的 Yield Index 自 2021 年以來跟蹤生態系收收益變化,顯示大多數主流資產和策略的可持續「核心收益」穩定在 5-15% 區間。這比早期大幅壓縮,但仍較傳統金融具明顯溢價優勢。)

Case Studies of Sustainable Yield Protocols

Examining specific protocols with demonstrated yield sustainability provides concrete evidence for the case that DeFi's high returns aren't merely a speculative bubble. These case studies illustrate how well-designed protocols can maintain attractive yields through genuine value creation rather than unsustainable mechanics.

(檢視一些已展現收益可持續性的協議,有助於證明 DeFi 高收益並非單純泡沫。這些案例說明精心設計的協議,如何透過真正的價值創造,而不是短暫的激勵,來維持具吸引力的回報。)

Curve Finance: The Stability King

Curve Finance has emerged as perhaps the most compelling example of sustainable yield generation in DeFi. Launched in 2020, Curve specializes in stable asset swaps, focusing on minimizing slippage for stablecoins and similar pegged assets.

(Curve Finance 堪稱 DeFi 可持續收益最具代表性的案例之一。自2020年推出以來,Curve 專注於穩定資產兌換,致力於將穩定幣等錨定資產的滑價降到最低。)

Curve's yield sustainability stems from multiple reinforcing mechanisms:

(Curve 的收益可持續性來自多重互補機制:)

- Trading fees: Liquidity providers earn from the platform's 0.04% fee on swaps

(交易手續費:流動性提供者獲得平台 0.04% 交易費分成) - CRV emissions: The protocol distributes CRV tokens to liquidity providers

(CRV 發放:協議向流動性提供者定期發放 CRV 代幣) - Vote-escrowed economics: Users can lock CRV for up to 4 years to receive veCRV

(投票鎖倉機制:用戶可鎖倉 CRV 最長4年換取 veCRV) - Bribes market: Third-party protocols pay veCRV holders to direct emissions

(賄賂市場:第三方協議向 veCRV 持有者支付費用,以爭取發放指向)

What makes Curve particularly notable is how these mechanisms create aligned incentives across stakeholders. Long-term believers lock their CRV for maximum voting power, reducing circulating supply while gaining control over the protocol's liquidity direction. This model has maintained competitive yields ranging from 5-20% annually on stablecoin pools even during extended bear markets.

(Curve 之所以突出,在於這些機制讓利害關係人利益高度一致。長期支持者鎖倉 CRV 獲取最大投票權,既能減少流通供給,又可掌控協議流動性導向。即使在熊市中,這一模式仍讓穩定幣池維持每年 5-20% 有競爭力收益。)

Aave: Institutional-Grade Lending

Aave represents another compelling example of sustainable yield generation in the lending sector. As one of DeFi's premier money markets, Aave allows users to deposit assets to earn interest while enabling others to borrow against collateral.

(Aave 則是借貸領域可持續收益的代表。作為 DeFi 主流貨幣市場之一,Aave 用戶可存入資產獲利息,亦能用資產作抵押進行借貸。)

Aave's yield sustainability derives from several key factors:

(Aave 的收益可持續性來自幾個關鍵要素:)

- Market-driven interest rates: Aave's utilization curve automatically adjusts rates based on supply and demand

(市場驅動利率:利用率曲線自動根據資金供需調整利率) - Risk-adjusted pricing: Different assets command different rates based on their risk profiles

(風險調整定價:不同資產根據其風險特徵收取不同利率) - Protocol fees: A small portion of interest payments goes to the protocol treasury and stakers

(協議費用:部分利息收入流向協議金庫與質押者) - Safety Module: AAVE token stakers provide insurance against shortfall events

(安全模組:AAVE 代幣質押者為潛在損失提供保險機制)

Aave's lending yields have demonstrated remarkable consistency, typically offering 3-8% on stablecoins and 1-5% on volatile assets across market cycles. These returns derive primarily from organic borrowing demand rather than token subsidies, creating a sustainable model that could theoretically operate indefinitely.

(Aave 借貸收益一貫穩健,穩定幣年化約 3-8%、波動資產約 1-5%,不論市場週期。這些收益主要來自真實借款需求,不依賴代幣補貼,具有理論上可永久運作的可持續性。)

Lido: Liquid Staking Dominance

Lido Finance has revolutionized Ethereum staking through its liquid staking derivatives model. By allowing users to stake ETH while receiving liquid stETH tokens that can be used throughout DeFi, Lido created a fundamentally sustainable yield source.

(Lido Finance 透過流動質押衍生品模式,徹底改變以太坊質押格局。用戶可質押 ETH 並取得可在全 DeFi 流通的 stETH,從根本上建立了一種可持續收益的模式。)

Lido's yields derive directly from Ethereum's protocol-level staking rewards - currently around 3-4% annually - with additional yield opportunities created through stETH's DeFi compatibility. This model creates sustainable yield without relying on token emissions or unsustainable incentives.

(Lido 的收益直接來自以太坊協議層質押獎勵,目前年化約 3-4%,且因 stETH 可於 DeFi 生態中靈活運用,帶來額外收益空間。該模式不依賴代幣發放或不可持續的激勵,實現了真正可持續的收益來源。)

The protocol has maintained consistent growth, capturing over 35% of all staked ETH by 2025, while offering yields that closely track Ethereum's base staking rate plus a premium for the liquid staking innovation. This demonstrates how infrastructural DeFi protocols can create sustainable yield advantages through genuine innovation rather than unsustainable tokenomics.

(Lido 協議持續成長,預計到 2025 年市佔全網質押 ETH 超過 35%,所提供收益緊貼以太坊質押基本利率,加上流動質押模式帶來的溢價,證明基礎設施級 DeFi 協議能以真正創新創造可持續收益,而非僅靠激勵設計撐場面。)

Risk-Adjusted Returns: A More Realistic Perspective

Comprehensive Risk Assessment

When evaluating DeFi yields, considering risk-adjusted returns provides a more accurate picture of sustainability than focusing solely on nominal APYs. Risk-adjusted metrics attempt to normalize yields based on their corresponding risk profiles, enabling fairer comparison between different opportunities.

(評估 DeFi 收益時,應重視風險調整後的回報,而非只看表面年化收益率(APY),如此才能更真實反映其可持續性。這類指標旨在根據風險特徵對收益進行標準化,方便更公平比較不同投資機會。)

Advanced risk-adjusted yield models calculate:

(進階的風險調整模型會計算以下指標:)

- Sharpe-like ratios: Yield excess over risk-free rate divided by yield volatility

(類夏普值:衡量收益相對無風險利率的超額報酬與波動比) - Sortino variations: Focusing specifically on downside risk rather than general volatility

(Sortino 指標變體:特別關注下行風險) - Maximum drawdown-adjusted returns: Yields normalized by worst historical performance

(最大回撤調整回報:根據歷史最差表現進行標準化) - Conditional value at risk: Accounting for tail risk beyond simple volatility measures

(條件風險價值(CVaR):涵蓋罕見極端波動造成的尾部風險) - Probability-weighted expected returns: Incorporating likelihood of different scenarios

(機率加權期望報酬:考量各種可能情境概率)

These metrics reveal which yields genuinely compensate for their associated risks versus those that appear attractive only by ignoring or underpricing their risk profiles. Analysis using these measures suggests that many apparently high-yielding opportunities actually offer poor risk-adjusted returns compared to more modest but sustainable alternatives.

(這些指標能顯示哪些收益真正反映風險、哪些則僅因低估或忽視風險而「看似高報酬」。相關分析也指出,很多表面高收益機會,經風險調整後其實遠遜於較為溫和但可持續的方案。)

Risk-adjusted yield aggregator DeFiSafety has compiled extensive data showing that after accounting for all risk factors, "true" sustainable DeFi yields likely fall in the 6-12% range for most strategies - significantly lower than advertised rates but still substantially higher than traditional alternatives.

(風險調整收益彙總平台 DeFiSafety 彙整大量數據顯示,全面考量各類風險後,多數 DeFi 策略的「真實」可持續收益應落在 6-12% 區間,雖明顯低於廣告標榜,但仍遠高於傳統金融。)

Risk Categories in DeFi

Advanced risk assessment models categorize DeFi risks into multiple dimensions, each with distinct implications for yield sustainability:

(進階風險評估還將 DeFi 風險細分為多重面向,每項對收益可持續性影響不一:)

Smart Contract Risk:

- Code vulnerability probability

(程式碼漏洞機率) - Historical audit quality

(過往審計品質) - Complexity metrics

(合約複雜度指標) - Dependencies on external protocols

(對外部協議的依賴)

Economic Design Risk:

- Tokenomic stability measurements

(代幣經濟穩定性評分) - Incentive alignment scores

(激勵一致性指標) - Game theory vulnerability assessment

(博弈論脆弱性分析) - Stress test simulation results

(壓力測試模擬結果)

Market Risk:

- Liquidity depth metrics

(流動性深度指標) - Correlation with broader markets

(對大盤市場的聯動性) - Volatility profiles

(波動性特徵) - Liquidation cascade vulnerability

(清算連鎖反應風險)

Operational Risk:

- Team experience evaluation

(團隊經驗評估) - Development activity metrics

(開發進度指標) - Community engagement measures

(社群活躍度評量) - Transparency indicators

(透明度檢核)

Regulatory Risk:

- Jurisdictional exposure analysis

(司法管轄區風險分析) - Compliance feature integration

(合規機制完善度) - Privacy mechanism assessment

(隱私機制評量) - Legal structure evaluation

(法律結構評估)

By quantifying these diverse risk categories, comprehensive frameworks create risk profiles for each protocol and yield source. These profiles enable calculation of appropriate risk premiums - the additional yield necessary to compensate for specific risks. This approach suggests that sustainable DeFi yields likely settle at levels providing reasonable compensation for their genuine risks - typically 3-10% above truly risk-equivalent traditional finance alternatives once all factors are properly accounted for.

(透過量化這些多元風險,可為每個協議及收益來源建立詳細風險評定,進而計算出對應風險溢價——即補償特定風險所需的額外收益。這種方法推論,可持續的 DeFi 收益率,應合理高於同等風險的傳統金融工具約 3-10% 左右,這是在全面納入所有風險後較為公允的水平。)

The Risk-Adjusted Yield Frontier

The concept of a "risk-adjusted yield frontier" helps visualize sustainable DeFi returns. This frontier represents the maximum theoretically achievable yield for any given risk level, with positions below the frontier indicating inefficiency and positions above suggesting unsustainable returns that will eventually revert.

(「風險調整收益前緣」的概念,有助於直觀理解可持續 DeFi 回報。它呈現每一風險水準下理論上可達到的最高回報;若落於前緣下方,代表資本配置無效率;高於前緣則意味該回報不可持續,終將回歸。)

Research by Gauntlet Networks, a leading DeFi risk modeling firm, has mapped this frontier across various DeFi strategies. Their analysis suggests that sustainable risk-adjusted yields in DeFi might exceed traditional finance by approximately:

(專業風險建模機構 Gauntlet Networks 針對各種 DeFi 策略繪製過該前緣。分析指出,DeFi 在風險調整後仍可比傳統金融高出:)

- 2-4% for conservative, secured lending strategies

(穩健型有抵押借貸:高出 2-4%) - 4-8% for liquidity provision in established markets

(主流市場流動性提供:高出 4-8%) - 8-15% for more complex, actively managed strategies

(複雜積極型策略:高出 8-15%)

These premiums derive from the fundamental efficiency and disintermediation advantages discussed earlier, suggesting that DeFi can maintain a sustainable yield advantage even after accounting for its unique risks. However, these premiums fall significantly short of the triple-digit APYs that initially attracted many participants to the ecosystem.

(這些溢價來自前述效率提升及去中介化的根本優勢,證明 DeFi 即使計入獨有風險後,仍可保持合理收益優勢。不過,相較於初期曾出現的三位數年化報酬,這顯然低了許多。)

The Integration of AI into DeFi's Future

AI-Driven Protocol Design

Looking toward the future, artificial intelligence is increasingly shaping how DeFi protocols are designed from the ground up. This integration promises to create more sustainable yield mechanisms by embedding intelligent systems directly into protocol architecture.

自基礎起塑造 DeFi 協議的設計方式。這種整合透過將智慧系統直接嵌入到協議架構中,有望創造出更具永續性的收益機制。

Several key developments are already emerging in 2025:

到了 2025 年,已有數項關鍵的發展逐漸浮現:

-

Adaptive Yield Parameters: Protocols using AI to dynamically adjust emission rates, fee distributions, and other yield-determining factors based on market conditions and sustainability metrics. These systems can respond to changing conditions much more effectively than traditional governance processes. Synthetix's Perceptron system, launched in late 2024, dynamically adjusts staking rewards to maximize protocol growth while ensuring economic sustainability.

-

自適應收益參數:協議運用 AI 根據市場狀況和永續性指標動態調整發放率、費用分配以及其他決定收益的因子。這些系統對於變動的條件能遠比傳統治理流程來得更有效果。例如 Synthetix 於 2024 年底推出的 Perceptron 系統,便能動態調整質押獎勵,在確保經濟永續性的同時,最大化協議成長。

-

Predictive Risk Management: AI systems embedded within lending and derivatives protocols to predict potential market dislocations and adjust collateralization requirements or liquidation thresholds preemptively, reducing systemic risks. For example, Gauntlet's Risk AI now powers risk parameters for over $15 billion in DeFi assets, using simulation-based machine learning to optimize for safety and capital efficiency.

-

預測性風險管理:AI 系統嵌入在借貸與衍生品協議中,能預測潛在市場失衡,並預先調整擔保品比率或清算門檻,降低系統性風險。以 Gauntlet 的 Risk AI 為例,目前已管理超過 150 億美元的 DeFi 資產風險參數,並透過模擬式機器學習優化安全性與資本效率。

-

Personalized Yield Strategies: Platforms offering AI-generated yield strategies tailored to individual user risk profiles, time horizons, and financial goals rather than one-size-fits-all approaches. DefiLlama's AI Advisor, launched in February 2025, analyzes users' portfolios and risk preferences to recommend personalized yield strategies across hundreds of protocols.

-

個人化收益策略:平台提供 AI 生成的收益策略,根據用戶個人風險承受度、投資期限與財務目標量身定制,而非一體適用的解決方案。例如 DefiLlama 於 2025 年二月推出的 AI Advisor,可分析用戶投資組合與風險偏好,針對數百種協議推薦個人化收益策略。

The integration of AI into protocol design represents a significant evolution beyond merely using AI for analysis. By embedding intelligence directly into the protocols themselves, DeFi systems can potentially create more sustainable and adaptable yield mechanisms that respond to changing conditions while maintaining appropriate risk parameters.

AI 的嵌入不僅僅侷限於分析,而是促使協議設計本身產生重大演進。將智慧直接注入協議本體,讓 DeFi 系統有機會設計出更永續且可調適的收益機制,在維持適當風險參數下應對環境變化。

AI Applications in DeFi Risk Assessment

AI 在 DeFi 風險評估的應用

Artificial intelligence has become an increasingly crucial tool for analyzing DeFi yield sustainability. As the ecosystem grows in complexity, AI's ability to process vast datasets and identify subtle patterns offers unprecedented insight into what yields might be sustainable long-term.

人工智慧已成為分析 DeFi 收益永續性的關鍵工具。隨著生態系複雜度提升,AI 處理龐大資料集與發掘細微模式的能力,提供了前所未有的洞見,協助判斷哪些收益具備長期永續性。

By 2025, AI has permeated virtually every aspect of DeFi operations and analysis. AI models now routinely evaluate protocol security risks by analyzing smart contract code, governance structures, and historical performance. Advanced systems can identify potential vulnerabilities that might escape human auditors by comparing new protocols against databases of previous exploits.

到了 2025 年,AI 幾乎滲透 DeFi 的所有操作與分析面向。AI 模型會經常性評估協議的安全風險,包括分析智慧合約原始碼、治理架構及歷史表現。先進的系統甚至能將新協議與過往漏洞資料庫比對,發現人類審計員可能忽略的潛在弱點。

These risk assessment capabilities have direct implications for yield sustainability. Machine learning algorithms can quantify previously subjective risk factors into concrete probability metrics, allowing for more accurate risk-adjusted yield calculations. For instance, AI systems regularly generate comprehensive risk scorecards for DeFi protocols that correlate strongly with subsequent exploit likelihood.

這些風險評估能力,對收益永續性有直接影響。機器學習可將以往主觀的風險因子量化為具體機率指標,讓收益風險調整計算更精確。例如,AI 系統能定期為 DeFi 協議產生風險評分表,其分數與日後被攻擊的風險高度相關。

A notable example is Consensys Diligence AI, which has analyzed over 50,000 smart contracts, identifying vulnerability patterns that have helped prevent an estimated $3.2 billion in potential losses. This security layer potentially enables higher sustainable yields by reducing the "security tax" discussed earlier.

值得一提的是 Consensys Diligence AI,已分析超過 5 萬份智慧合約,找出漏洞模式,協助預防約 32 億美元的潛在損失。這一層的安全保障,能降低前述的「安全稅」,進而提升可持續收益。

Yield Optimization Through Machine Learning

透過機器學習最佳化收益

Perhaps the most visible application of AI in DeFi comes in the form of increasingly sophisticated yield optimization strategies. Modern yield aggregators employ machine learning to:

AI 在 DeFi 最顯著的應用,莫過於日益複雜的收益最佳化策略。現代收益聚合器運用機器學習來:

- Predict short-term yield fluctuations across protocols

預測各協議短期收益波動 - Identify optimal entry and exit points for various strategies

辨識不同策略的最佳進出點 - Balance risk factors against potential returns

在風險與報酬之間尋求最佳平衡 - Optimize gas costs and transaction timing

最佳化 gas 費用與交易時機

Platforms like Yearn Finance now employ advanced AI to manage billions in assets, automatically shifting capital between opportunities based on complex models that consider dozens of variables simultaneously. These systems have demonstrated an ability to generate returns 2-3% higher annually than static strategies by capitalizing on yield inefficiencies before they're arbitraged away.

像 Yearn Finance 等平台,現已用先進 AI 管理數十億資產,依據納入數十項變數的複雜模型,自動調整資本於不同機會之間。這些系統能捕捉尚未被套利的收益低效率,每年創造比靜態策略高出 2-3% 的報酬。

The consensus from advanced yield prediction models suggests several important conclusions regarding sustainability:

來自先進收益預測模型的共識指出,關於永續性有幾點關鍵結論:

- Base yield layers: Models identify persistent "base layers" of sustainable yield across various DeFi categories, typically 3-7% above traditional finance alternatives.

基礎收益層:模型辨識出在多種 DeFi 類別中可持續存在的「基礎收益層」,一般比傳統金融高 3-7%。 - Protocol maturation curves: Models characterize the typical yield compression curve as protocols mature.

協議成熟曲線:模型能描繪協議隨著成熟而出現的典型收益壓縮曲線。 - Sustainability thresholds: AI systems identify critical thresholds in metrics like emissions-to-revenue ratio that strongly predict long-term yield viability.

永續性門檻:AI 系統可找出如「發放對收入比」一類的重要指標臨界值,精準預測長期收益可行性。 - Risk premiums: Models quantify the appropriate risk premium for different protocol categories, distinguishing between justified high yields and unsustainable returns.

風險溢酬:模型量化不同協議類型的適當風險溢酬,協助分辨合理高收益與不可持續的高報酬。

DefiAI Research has developed comprehensive models suggesting that AI-optimized strategies could maintain a 4-8% yield advantage over traditional finance indefinitely through efficiency gains and continuous optimization across the DeFi ecosystem.

DefiAI Research 開發出完整的模型,顯示透過效率提升與 DeFi 生態持續優化,AI 最佳化策略可長期維持比傳統金融高出 4-8% 的收益優勢。

Pattern Recognition and Anomaly Detection

模式識別與異常偵測

Beyond basic prediction, advanced AI systems excel at identifying subtle patterns and anomalies within DeFi yield data that provide insight into sustainability questions. These capabilities enable researchers to detect unsustainable yield mechanisms before they collapse and identify truly innovative models that might sustain higher returns.

除基本預測能力外,先進 AI 系統更擅長在 DeFi 收益資料中識別隱微模式與異常,有助於剖析永續性相關議題。這些能力讓研究人員能在收益機制崩解前預先察覺不永續的徵兆,或發掘真正創新的高報酬模式。

AI research has identified several distinct yield patterns that correlate strongly with sustainability outcomes:

AI 研究已識別出若干與永續性高度相關的收益模式:

- Sustainable Yield Pattern: Characterized by moderate baseline returns (5-15%), low volatility, minimal correlation with token price, and strong connection to protocol revenue.

可持續收益模式:具備中等基礎報酬(5-15%)、低波動、與代幣價格關聯性低、且與協議收入高度連結的特性。 - Emissions-Dependent Pattern: Marked by high initial yields that progressively decrease following a predictable decay curve as token emissions reduce or token price falls.

發放依賴型模式:以高初始收益為特徵,隨發放量減少或幣價下跌依可預期衰減曲線持續降低。 - Ponzi Pattern: Identified by yields that increase with new capital inflows but lack corresponding revenue growth.

龐氏型模式:收益隨新資金流入而升高,但缺乏相應收入增長。 - Innovation-Driven Pattern: Distinguished by initially high but eventually stabilizing yields as a truly innovative mechanism finds its market equilibrium.

創新驅動型模式:開始時收益較高,之後隨創新機制達到市場均衡而逐漸穩定。

By combining pattern recognition and anomaly detection, AI researchers have developed effective early warning systems for unsustainable yield mechanisms. These systems monitor the DeFi ecosystem for signs of yield patterns that historically preceded collapses or significant contractions.

透過融合模式識別與異常偵測,AI 研究者建立出有效的永續性預警系統。這些系統持續監控 DeFi 生態,蒐集過去在崩潰或大幅收縮前常見的收益模式徵兆。

ChainArgos, a leading blockchain analytics platform, has developed AI models that successfully predicted major yield collapses in protocols like MetaVault and YieldMatrix weeks before their public implosions. This predictive capability offers a potential path to more sustainable DeFi participation by allowing investors to avoid unsustainable yield traps.

領先的區塊鏈分析平台 ChainArgos 所開發的 AI 模型,能在像 MetaVault、YieldMatrix 等協議公開爆雷前數週成功預測其收益崩盤。這種預測能力為更永續的 DeFi 參與帶來契機,使投資者能有效避開不可持續的收益陷阱。

The Emergence of Real Yield

「真實收益」的興起

From Emissions to Revenue

從發放走向收入

The concept of "real yield" has emerged as a crucial distinction in assessing DeFi sustainability. Real yield refers to returns derived from actual protocol revenue and usage fees rather than token emissions or other potentially unsustainable sources.

「真實收益」逐漸成為評判 DeFi 永續性的關鍵標準。真實收益是指來自協議實際收入與手續費的報酬,而非來自代幣發放或其他可能不可持續的來源。

In the early days of DeFi, most yields were heavily dependent on token emissions - protocols distributing their governance tokens to attract liquidity and users. While this approach successfully bootstrapped the ecosystem, it inevitably led to token dilution and yield compression as emissions continued. The mathematical reality of token emissions means they cannot sustain high yields indefinitely unless matched by corresponding growth in protocol value and utility.

在 DeFi 發展初期,多數收益嚴重依賴代幣發放—協議發放治理代幣以吸引流動性和用戶。雖然這種方式成功啟動生態,但隨著持續發放,最終導致代幣稀釋和收益壓縮。數學上的現實是,除非協議價值及實用性同步成長,否則僅靠發放無法長期維持高額收益。

By 2025, many leading protocols have successfully transitioned toward real yield models where returns come predominantly from:

到了 2025 年,許多主流協議已成功轉型為真實收益模式,主要收益來源包括:

- Trading fees on decentralized exchanges

去中心化交易所的交易手續費 - Interest paid by borrowers on lending platforms

借貸平台中借款人支付的利息 - Liquidation fees from collateralized positions

擔保倉位的清算手續費 - Premium payments for risk protection

風險保障的保費收入 - Protocol revenue sharing mechanisms

協議收益分潤機制

This transition marks a critical maturation of the DeFi ecosystem. While real yields are typically lower than the eye-catching numbers seen during emission-heavy periods, they represent fundamentally more sustainable return sources. Protocols generating significant revenue relative to their token emissions demonstrate much greater yield stability across market cycles.

這項轉型標誌著 DeFi 生態的重要成熟。雖然真實收益通常低於發放盛行時期的高額數據,但其本質上更具永續性。協議若能創造高於代幣發放水準的實質收入,則在市場週期間會展現出更穩定的收益。

DeFi Pulse's Real Yield Index, launched in October 2024, tracks yields derived solely from protocol revenues across the ecosystem. Their analysis shows that real yields across major DeFi protocols averaged 7.3% in Q1 2025—significantly lower than advertised rates but still substantially higher than comparable traditional finance alternatives.

2024 年 10 月上線的 DeFi Pulse 真實收益指數,即追蹤整體生態中的「純協議收入」型收益。其分析指出,2025 年第一季主要 DeFi 協議平均真實年化收益為 7.3%,雖低於不少宣傳數據,但仍遠高於傳統金融同類產品。

The Buy-Back and Revenue-Sharing Model

回購與收入分潤模式

A particularly promising development in sustainable yield generation is the rise of protocols that share revenue directly with token holders through systematic token buy-backs and revenue distribution. This model creates a transparent, auditable yield source tied directly to protocol performance.

在可持續收益生成方面,一個特別有潛力的發展是,協議直接透過系統性代幣回購與收入分配,把協議收益返還給持幣人。此機制建立出透明且可審計、與協議實績直接連動的收益來源。

Leading examples of this approach include:

這種模式的知名案例包括:

- GMX: This decentralized perpetual exchange distributes 30% of trading fees to esGMX stakers and another 30% to GLP liquidity providers, creating sustainable yields backed directly by platform revenue

GMX:此去中心化永續合約交易所,將 30% 交易手續費分配給 esGMX 質押者,另 30% 分配給 GLP 流動性供應者,收益直接來自平台營收,實現可持續收益 - Gains Network: Their synthetic trading platform shares 90% of trading fees with liquidity providers and governance token stakers

Gains Network:該合成交易平台將 90% 交易手續費返還給流動性供應者與治理代幣質押者 - dYdX: Their v4 chain implements an automatic buy-back and distribution mechanism that returns trading revenue to governance token stakers

dYdX:v4 版區塊鏈實作自動回購與分配機制,將交易收入回饋給治理代幣持有者

These revenue-sharing mechanisms represent perhaps the most sustainable yield models in DeFi, as they directly link returns to genuine economic activity rather than unsustainable token emissions. While yields from these mechanisms typically range from 5-20% rather than the triple-digit returns seen in emission-heavy models, they demonstrate

這些收入分潤機制,也許是 DeFi 當下最永續的收益模式,因為它們讓報酬直接綁定真實經濟活動,而非不可持續的代幣發放。雖然這些協議的收益率通常介於 5~20%,而非高達三位數的發放型模式,但其所展現的永續性與穩定性,...much greater stability across market cycles.

TokenTerminal data shows that revenue-sharing protocols maintained relatively stable yield distributions throughout both bull and bear market conditions in 2023-2025, suggesting this model might represent a truly sustainable approach to DeFi yield generation.

TokenTerminal data 顯示,收益分享協議在 2023-2025 年的牛市與熊市期間,都能維持相對穩定的收益分配,這顯示此類模式有可能是一種真正可持續的 DeFi 收益生成方法。

Real-World Asset Integration

Perhaps the most significant development in sustainable DeFi yield generation is the integration of real-world assets (RWAs) into the ecosystem. By connecting DeFi liquidity with tangible economic activity beyond the crypto sphere, RWA protocols create yield sources backed by genuine economic productivity rather than speculative mechanisms.

或許在可持續 DeFi 收益生成方面,最重大的發展就是將現實世界資產(RWA)整合進生態系。RWA 協議將 DeFi 流動性與加密貨幣圈以外的實體經濟活動連結起來,創造由真正經濟生產力所支持的收益來源,而非僅倚賴投機性機制。

The RWA sector has grown exponentially, from under $100 million in 2021 to over $50 billion by early 2025, according to RWA Market Cap. This growth reflects increasing recognition that sustainable yields ultimately require connection to real economic value creation.

根據 RWA Market Cap,RWA 產業已呈現指數型成長,從 2021 年的不到一億美元成長到 2025 年初已突破五百億美元。這種成長代表市場愈來愈明白,真正可持續的收益終須與實體經濟價值創造相連結。

Major RWA yield sources now include:

- Tokenized Treasury Bills: Protocols like Ondo Finance and Maple offer yields backed by U.S. Treasury securities, providing DeFi users access to sovereign debt yields plus a small premium for the tokenization service

- Private Credit Markets: Platforms like Centrifuge connect DeFi liquidity with SME financing, invoice factoring, and other private credit opportunities

- Real Estate Yields: Projects like Tangible and RealT tokenize property income streams, enabling DeFi users to access real estate yields

- Carbon Credits and Environmental Assets: Protocols like KlimaDAO generate yields through environmental asset appreciation and impact investing

目前主要的 RWA 收益來源包括:

- 代幣化國債:如 Ondo Finance 和 Maple 等協議提供以美國國債為基礎資產的收益,讓 DeFi 用戶得以取得主權債收益及代幣化服務的小額溢價

- 私人信貸市場:如 Centrifuge 等平台將 DeFi 流動性導入中小企業融資、發票貼現及其他私募信貸機會

- 不動產收益:Tangible 和 RealT 等專案將不動產的收益流代幣化,使 DeFi 用戶能夠取得房地產相關收益

- 碳權與環境資產:如 KlimaDAO 等協議透過環境資產增值及影響力投資來創造收益

These RWA yield sources typically offer returns ranging from 3-12% annually—less spectacular than some native DeFi opportunities but generally more sustainable and less volatile. Their growing integration with traditional DeFi creates a promising path toward long-term yield sustainability by anchoring returns to fundamental economic value.

這些 RWA 收益來源年化回報率一般介於 3-12%,雖不如部分原生 DeFi 項目那麼驚人,但普遍更具可持續性與穩定性。隨著它們與傳統 DeFi 的結合日益緊密,為長期收益可持續性打下根基,讓回報更貼近經濟基本面。

The recent BlackRock tokenized securities partnership with several DeFi platforms marks mainstream financial validation of this approach, potentially accelerating the integration of traditional financial yields into the DeFi ecosystem.

最近 BlackRock 與多個 DeFi 平台的代幣化證券合作,象徵主流金融界對此模式的肯定,也有望加速將傳統金融收益納入 DeFi 生態系。

Institutional Perspectives on DeFi Yields

Traditional Finance Adoption Patterns

The relationship between traditional financial institutions and DeFi has evolved dramatically since 2020. Early institutional engagement was primarily exploratory, with most established players maintaining skeptical distance from the volatile, unregulated ecosystem. By 2025, institutional adoption has accelerated significantly, providing important signals about which yield sources sophisticated investors consider sustainable.

自 2020 年以來,傳統金融機構與 DeFi 的關係出現了重大演變。早期機構多以探索性質參與,大多數成熟機構對於這個波動且未受規管的生態系態度保留。到了 2025 年,機構級採納大幅加速,清楚反映資深投資人認可哪些收益來源是可持續的。

Several distinct institutional adoption patterns have emerged:

- Conservative Bridging: Institutions like BNY Mellon and State Street have established conservative DeFi exposure through regulated staking, tokenized securities, and permissioned DeFi instances, targeting modest yield premiums (2-5%) with institutional-grade security

- Dedicated Crypto Desks: Investment banks including Goldman Sachs and JPMorgan operate specialized trading desks that actively participate in sustainable DeFi yield strategies, particularly in liquid staking derivatives and RWA markets

- Asset Manager Integration: Traditional asset managers like BlackRock and Fidelity have integrated select DeFi yield sources into broader alternative investment offerings, focusing on opportunities with transparent revenue models

目前有三大明顯的機構採用路徑:

- 保守型橋接:像 BNY Mellon、State Street 等機構,透過受監管質押、代幣化證券,以及有權限限制的 DeFi 服務,建立保守 DeFi 部位,鎖定 2-5% 的溫和收益溢價,同時擁有機構級安全性

- 專業加密部門:如高盛與摩根大通等投資銀行設有專門的加密貨幣交易部門,積極參與可持續 DeFi 收益策略,尤其是在流動質押衍生品和 RWA 市場

- 資產管理結合:BlackRock、Fidelity 等傳統資產管理公司,將特定 DeFi 收益來源納入更廣泛的另類投資產品組合,聚焦於盈收模式透明的機會

Particularly notable is the launch of JPMorgan's Tokenized Collateral Network, which incorporates DeFi mechanisms while meeting regulatory requirements. This initiative signals institutional recognition that certain DeFi yield innovations offer sustainable efficiency improvements over traditional alternatives.

特別值得注意的是 摩根大通的代幣化抵押品網路 啟動,該平台結合 DeFi 機制,同時符合監管要求。這一舉措代表機構層面認可部分 DeFi 收益創新能帶來可持續且高效的優勢,優於傳統選擇。

Institutional Risk Assessment Frameworks

Institutional investors have developed sophisticated frameworks for evaluating which DeFi yields might prove sustainable long-term. These frameworks provide valuable insight into how professional risk managers distinguish between sustainable and unsustainable return sources.

機構投資人已發展出精密的框架,評估哪些 DeFi 收益有長期可持續性。這些框架透露了專業風控人員如何區分可持續與不可持續的收益來源。

Galaxy Digital's DeFi Risk Framework, published in March 2025, offers a comprehensive methodology incorporating:

- Protocol Risk Tiering: Categorizing protocols from Tier 1 (highest security, longest track record) to Tier 4 (experimental, unaudited), with explicit limits on exposure to lower tiers

- Yield Source Analysis: Classifying yield sources as either "fundamental" (derived from genuine economic activity) or "incentive" (derived from token emissions), with strong preference for the former

- Composability Risk Mapping: Tracing dependencies between protocols to quantify systemic exposure

- Regulatory Compliance Scoring: Evaluating protocols based on their compatibility with evolving regulatory requirements

Galaxy Digital 在 2025 年 3 月公布的 DeFi 風險評估框架,提出一整套詳細方法論,包括:

- 協議風險分級:將協議區分為從一級(安全性最高、歷史最久)到四級(實驗性、未經審計),並嚴格限制低級別曝險

- 收益來源分析:將收益來源分為「基本型」(來自真實經濟活動)或「激勵型」(來自代幣發放),並明確偏好前者

- 可組合風險圖譜:追蹤協議間依賴關係,量化系統性曝險

- 法規合規性評分:依協議對最新監管要求的相容程度評分

The framework concludes that institutionally acceptable sustainable yields likely range from 2-4% above traditional alternatives for Tier 1 protocols, with progressively higher yields required to compensate for additional risk in lower tiers.

此框架評估,一級協議的可持續收益,機構普遍可接受落在傳統選擇之上 2-4%;若風險階層降低,則必須對應更高的風險要求更高的回報。

Institutional Capital Flows and Market Impact

The patterns of institutional capital allocation provide perhaps the most concrete evidence regarding which DeFi yields professional investors consider sustainable. By tracking where sophisticated capital flows, we can identify which yield mechanisms demonstrate staying power beyond retail speculation.

機構資本的配置路徑,或許是專業投資人如何認定 DeFi 收益持久性的最明確證據。透過觀察大資金流向哪些區塊,就能發現哪些收益機制具備超越一般散戶投機的生命力。

According to Chainalysis's 2025 Institutional DeFi Report, institutional capital has concentrated heavily in several key segments:

- Liquid Staking Derivatives: Capturing approximately 40% of institutional DeFi exposure, with Lido Finance and Rocket Pool dominating

- Real World Assets: Representing 25% of institutional allocation, primarily through platforms offering regulatory-compliant tokenized securities

- Blue-Chip DEXs: Comprising 20% of institutional activity, focused on major venues with demonstrated revenue models

- Institutional DeFi Platforms: Capturing 15% of flows through permissioned platforms like Aave Arc and Compound Treasury

根據 Chainalysis 2025 年機構 DeFi 報告,機構資本主要集中於幾個重要領域:

- 流動質押衍生品:約 40% 的機構 DeFi 部位位於此區塊,Lido Finance 和 Rocket Pool 居主導地位

- 現實世界資產:約佔 25%,主力是合規代幣化證券平台

- 藍籌 DEXs:約佔 20%,聚焦於收入模式成熟且可驗證的大型交易平台

- 機構級 DeFi 平台:如 Aave Arc、Compound Treasury,約佔 15%

Notably absent from significant institutional allocation are the high-APY farming opportunities and complex yield aggregators that dominated retail interest in earlier cycles. This allocation pattern suggests professional investors have identified a subset of DeFi yield sources they consider fundamentally sustainable, while avoiding those dependent on speculative dynamics or unsustainable tokenomics.

明顯缺席於機構資本配置的,則是過去零售市場熱門的高 APY 挖礦專案與複雜型收益聚合器。此一配置模式說明,專業投資人已掌握哪些 DeFi 收益來源屬於基本面支撐的可持續機制,並避開依賴投機或不可持續代幣經濟的項目。

The March 2025 announcement that Fidelity's Digital Assets division had allocated $2.5 billion to DeFi strategies - focusing exclusively on what it termed "economically sustainable yield sources" - represents perhaps the strongest institutional validation of DeFi yield sustainability to date.

2025 年 3 月 Fidelity 宣布,其數位資產部門投入 25 億美元於 DeFi 策略,且僅聚焦其稱之為「經濟上可持續的收益來源」。這可能是至今最有力的機構層級對 DeFi 收益可持續性的背書。

The Yield Farming 2.0 Evolution

Sustainable Yield Farming Strategies

The DeFi ecosystem has witnessed a significant maturation in yield farming approaches since the initial "DeFi Summer" of 2020. This evolution, sometimes termed "Yield Farming 2.0," emphasizes sustainability, risk management, and genuine value creation over unsustainable token incentives.

自 2020 年的「DeFi 夏天」以來,DeFi 生態的收益農耕策略大幅成熟。這種被稱為「收益農耕 2.0」的演變,強調可持續性、風險管理與真實價值創造,而非僅憑不可持續的代幣激勵。

Key characteristics of these sustainable yield strategies include:

- Diversification Across Yield Sources: Modern yield farmers typically spread capital across multiple uncorrelated yield sources rather than concentrating in single high-APY opportunities, reducing specific protocol risk

- Revenue-Focused Selection: Prioritizing protocols with strong revenue models where yields derive primarily from fees rather than token emissions

- Strategic Position Management: Actively managing positions to minimize impermanent loss and maximize capital efficiency rather than passive "set and forget" approaches

- Risk-Adjusted Targeting: Setting realistic yield targets based on comprehensive risk assessment rather than chasing outlier APYs

這類可持續收益策略的主要特徵包括:

- 收益來源分散:現代收益農夫大都將資本分散於多個收益來源,避免單一高 APY 專案集中曝險,降低協議特定風險

- 盈收導向選擇:優先挑選營收結構強健、收益主要來自協議手續費而非代幣發放的項目

- 策略性部位管理:主動管理部位以減少無常損失並強化資本效率,而非被動「放著不管」

- 風險調整目標:根據完整風險評估,設定務實的收益目標,而非追逐極端高 APY

These evolutionary changes have created yield farming approaches with substantially different risk-return profiles compared to earlier generations. While Yield Farming 1.0 often produced spectacular but ultimately unsustainable returns through aggressive token emissions, Yield Farming 2.0 typically generates more modest but sustainable yields through genuine value capture.

這些革新大幅改變了收益農耕的風險/報酬特性。1.0 時代常靠激進的代幣發放創造高額但不可持續的回報;2.0 時代則多數透過真實價值捕捉,帶來較溫和但能長存的收益。

The rising popularity of platforms like DefiLlama Yield, which explicitly separates "Farm APR" (token emissions) from "Base APR" (genuine protocol revenue), demonstrates growing retail awareness of these sustainability distinctions.

像 DefiLlama Yield 這類新平台人氣漸高,該平台明確區分「農耕 APR」(代幣發放)與「基礎 APR」(協議營收),可見市場對收益可持續性的意識顯著提升。

Quantitative Yield Optimization

A significant development in sustainable yield farming has been the rise of quantitative approaches to yield optimization. These strategies apply mathematical models and algorithmic execution to maximize risk-adjusted returns while minimizing downside risks.

在可持續收益農耕領域,定量化收益優化的崛起是一大進展。這類策略運用數學模型與演算法交易,在降低下檔風險的同時最大化風險調整後的回報。

Leading quantitative yield strategies now include:

- Dynamic LTV Management: Algorithms that continuously optimize loan-to-value ratios in lending protocols based on volatility predictions, maximizing capital efficiency while minimizing liquidation risk

- Impermanent Loss Hedging: Sophisticated strategies that use options, futures, or other derivatives to hedge against impermanent loss in liquidity provision

- Yield Curve Arbitrage: Exploiting inefficiencies across lending protocols' interest rate curves through strategic borrowing and lending

- MEV Protection: Implementing transaction execution strategies that protect against miner/validator extractable value,

現今領先的量化收益策略包括:

- 動態 LTV 管理:利用演算法根據波動率預測,持續於借貸協議最佳化質押比(LTV),兼顧資本效率並降低被清算風險

- 無常損失避險:以選擇權、期貨或其他衍生品,針對流動性提供的無常損失進行高級對沖策略

- 收益曲線套利:透過策略性借貸,把握各借貸協議之間利率曲線的低效地帶

- MEV 保護:執行交易策略以防範礦工/驗證者可提取價值(MEV)損失preserving yields that would otherwise be captured by front-runners

保全原本可能被「搶先交易者」攫取的收益

These quantitative approaches have demonstrated ability to generate 3-5% additional annual yield compared to passive strategies, potentially enhancing the sustainable yield frontier. Platforms like Exponential and Ribbon Finance have pioneered these strategies, bringing sophisticated quantitative finance techniques to DeFi yield optimization.

這些量化方法已經展現出相較於被動策略能額外帶來3-5%的年化收益,有機會提升可持續收益的上限。像 Exponential 和 Ribbon Finance 等平台率先推出這些策略,把精密的量化金融技術引入 DeFi 收益優化領域。

Governance-Based Yield Mechanisms

The evolution of protocol governance has created entirely new yield mechanisms based on controlling protocol resources and directing incentives. These governance-based yields represent a distinct category that potentially offers sustainable returns through strategic influence rather than passive capital provision.

協議治理的演進催生了全新型態的收益機制,這類收益是透過控制協議資源和引導激勵結構產生。治理型收益屬於獨立的一大類別,其可望透過策略性影響力(而非單純被動資本參與)實現可持續的報酬。

The most sophisticated governance-based yield strategies involve:

最先進的治理型收益策略包括:

-

Vote-Escrow Models: Locking tokens for extended periods to gain boosted yields and governance power, pioneered by Curve and adopted by numerous protocols

-

鎖倉投票模型(Vote-Escrow Models):將代幣長期鎖定以獲得收益加成及治理權力,此模式由 Curve 首創,並被眾多協議採用。

-

Bribe Markets: Platforms where protocols compete for governance influence by offering rewards to governance token holders, creating additional yield layers

-

賄選市場(Bribe Markets):不同協議在這類平台上競逐治理影響力,通過向治理代幣持有人提供獎勵來創造額外的收益層次。

-

Treasury Management: Participating in governance to influence protocol treasury investments, potentially generating sustainable returns from productive asset allocation

-

國庫管理(Treasury Management):參與協議治理以影響國庫投資方向,透過有效配置資產來創造可持續收益。

-

Strategic Parameter Setting: Using governance rights to optimize protocol parameters for yield generation while maintaining system stability

-

策略參數設定(Strategic Parameter Setting):運用治理權利,優化協議參數以兼顧系統穩定與收益生成。

The Convex and Aura ecosystems exemplify how governance-based yields can create sustainable return sources by efficiently coordinating governance power across multiple protocols. These mechanisms create value through coordination efficiencies rather than unsustainable token emissions, potentially representing more durable yield sources.

Convex 及 Aura 等生態系統說明了治理型收益如何能透過多協議間高效協作治理權力,進而創造可持續收益來源。這些機制的價值來自協同效率,而非不可持續的代幣排放,因此更有機會成為長久的收益來源。

The Long-Term Outlook: Convergence or Disruption?

長期展望:融合還是顛覆?

The Sustainable Yield Equilibrium Hypothesis

可持續收益均衡假設

As DeFi matures, an important question emerges: will yields eventually converge with traditional finance or maintain a persistent premium? The Sustainable Yield Equilibrium Hypothesis proposes that after accounting for all relevant factors, DeFi yields will settle at levels moderately higher than traditional finance counterparts due to genuine efficiency advantages, but significantly lower than early-phase returns.

隨著 DeFi 發展日益成熟,一個重要問題逐漸浮現:DeFi 收益最終會與傳統金融趨於一致,還是持續保有溢價?可持續收益均衡假設認為,在考慮所有重要因素後,DeFi 的收益將因其確實的效率優勢,而保持比傳統金融略高的水平,但顯著低於創始早期的報酬。

The hypothesis suggests three distinct yield components:

此假設將收益拆解成三大成分:

-

Efficiency Premium: A sustainable 2-5% yield advantage derived from blockchain's technical efficiencies and disintermediation benefits

-

效率溢價(Efficiency Premium):來自區塊鏈技術效率與去中介化帶來的可持續2-5%收益優勢

-

Risk Premium: An additional 1-8% required to compensate for DeFi's unique risks, varying by protocol maturity and security profile

-

風險溢價(Risk Premium):為補償 DeFi 特有的風險(依協議成熟度和安全性而異),所需額外1-8%的收益

-

Speculative Component: A highly variable and ultimately unsustainable component driven by token emissions and market sentiment

-

投機成分(Speculative Component):受代幣排放及市場情緒驅動,變異大且最終不可持續的一環

Under this framework, only the first component represents a truly sustainable advantage, while the second appropriately compensates for additional risk rather than representing "free yield." The third component - which dominated early DeFi returns - gradually diminishes as markets mature and participants develop more sophisticated risk assessment capabilities.

在這個框架下,只有第一項效率溢價是真正可持續的優勢;第二項風險溢價實則是對額外風險的合理補償,並非「免費收益」;第三項投機成分——早期 DeFi 著重的來源——將隨著市場成熟、參與者風險評估精進而逐漸削減。

Research by the DeFi Education Fund examining yield trends from 2020-2025 supports this hypothesis, showing progressive compression toward an apparent equilibrium approximately 3-7% above traditional finance alternatives for risk-comparable activities.

The Institutional Absorption Scenario

機構吸納情境

An alternative view suggests that as traditional financial institutions increasingly absorb DeFi innovations, the yield gap may narrow more significantly through a process of institutional adoption and regulatory normalization.

另一種觀點指出,隨著傳統金融機構不斷吸收 DeFi 創新,借由機構採用和監管規範化,收益差距可能會明顯縮小。

Under this scenario, major financial institutions gradually integrate the most efficient DeFi mechanisms into their existing operations, capturing much of the efficiency premium for themselves and their shareholders rather than passing it to depositors or investors. Simultaneously, regulatory requirements standardize across traditional and decentralized finance, eliminating regulatory arbitrage advantages.

在這種情況下,大型金融機構會逐步將最具效率的 DeFi 機制納入原有營運,將效率溢價集中於自身及其股東,而非直接回饋給存戶或投資人。同時,監管規範會逐漸統一於傳統與去中心化金融之間,消除監管套利的優勢。

This process has already begun with initiatives like Project Guardian, a partnership between the Monetary Authority of Singapore and major financial institutions to integrate DeFi mechanisms into regulated financial infrastructure. Similar projects by central banks and financial consortia worldwide suggest accelerating institutional absorption.

此過程已因新加坡金管局與各大金融機構合作推動的 Project Guardian 等項目啟動,目的便是將 DeFi 機制納入受監管之金融基礎建設。全球各國央行與金融聯盟也發起類似計畫,反映機構吸納有加速趨勢。

If this scenario predominates, sustainable DeFi yields might ultimately settle just 1-3% above traditional alternatives - still representing an improvement, but less revolutionary than early adopters envisioned.

若此模式成為主流,則 DeFi 可持續收益最終可能僅比傳統金融略高1-3%,雖仍具優勢,但遠不及早期參與者期待的顛覆性。

The Innovation Supercycle Theory

創新超級循環理論

A more optimistic perspective is offered by the Innovation Supercycle Theory, which suggests that DeFi represents not merely an incremental improvement over traditional finance but a fundamental paradigm shift that will continue generating new yield sources through successive waves of innovation.

較為樂觀的觀點——創新超級循環理論——認為 DeFi 不只是在傳統金融基礎上的小幅進化,而是根本性的典範轉移,將藉由持續不斷的創新循環,源源不絕地創造新型收益來源。

Proponents of this view point to historical precedents in technological revolutions, where early innovations created platforms for successive waves of new development, each generating distinct value propositions. They argue that DeFi's composable, permissionless nature will continue spawning novel financial primitives that create genuinely sustainable yield sources unforeseen by current models.

持這一觀點的學者指出,歷史上的技術革命早期創新往往鋪墊了後續一波波發展,每一輪都產生全新價值主張。他們認為,DeFi 的可組合性和無需許可特質,將不斷孕育出新型金融原語,創造當前模型所無法預見的可持續收益來源。

Evidence for this theory includes the rapid emergence of entirely new financial categories within DeFi:

這一理論的佐證包括 DeFi 快速冒出的多種嶄新金融類型:

-

Liquid staking derivatives emerged in 2021-2022

-

流動質押衍生品於2021-2022年間崛起

-

Real-world asset tokenization gained significant traction in 2023-2024

-

實體資產代幣化在2023-2024年大幅成長

-

AI-enhanced DeFi protocols began delivering measurable value in 2024-2025

-

人工智慧加持的 DeFi 協議於2024-2025年開始創造可衡量價值

Each innovation cycle has created new yield sources not directly comparable to traditional finance alternatives. If this pattern continues, DeFi could maintain a substantial yield advantage through continuous innovation rather than settling into equilibrium with traditional systems.

每一次創新循環都帶來無法直接與傳統金融對應的新收益來源。若這一趨勢持續,DeFi 有機會藉著連續創新長期維持高於傳統體系的收益優勢,而非回歸均衡狀態。

MakerDAO's recent paper argues that we're currently witnessing just the third major innovation wave in DeFi, with at least four additional waves likely over the coming decade, each potentially creating new sustainable yield sources through fundamental innovation rather than unsustainable tokenomics

Final thoughts

最後思考

The question of DeFi yield sustainability defies simple answers. The evidence suggests that while many early yield mechanisms were fundamentally unsustainable, built on temporary token incentives and speculative dynamics, the ecosystem has evolved toward more durable models based on genuine efficiency advantages, disintermediation benefits, and innovative financial primitives.

DeFi 收益是否可持續,並無簡單答案。當前各種證據顯示,雖然早期收益機制多半基於臨時代幣激勵和投機動能,根本上難以維繫,但生態系已逐步走向以真正效率優勢、去中介化與嶄新金融原語為核心的長效機制。

The most likely outcome involves stratification across the ecosystem:

最可能出現的結局將是整個生態系的收益分層:

-

Core DeFi Infrastructure: Established protocols like Curve, Aave, and Lido will likely continue offering sustainable yields 3-7% above traditional finance alternatives, derived from genuine efficiency advantages and reasonable risk premiums.

-

核心 DeFi 基礎設施:如 Curve、Aave、Lido 等老牌協議,預計將繼續提供高於傳統金融3-7%的可持續收益,主要來自效率優勢與合理風險溢價。

-

Innovation Frontier: Emerging protocol categories will continue generating temporarily higher yields during their growth phases, some of which will evolve into sustainable models while others collapse when unsustainable mechanisms inevitably fail.

-

創新前沿:新興協議類型在成長階段會持續產生短暫高收益,其中部分能轉化為可持續機制,其餘則隨著不可持續結構崩潰而消失。

-

Institutional DeFi: A growing regulated segment will offer yields 1-3% above traditional alternatives, with enhanced security and compliance features targeting institutional participants unwilling to accept full DeFi risk exposure.

-

機構級 DeFi:這一受監管的領域將提供高於傳統金融1-3%的收益,並強化安全與合規設計,針對不願承擔 DeFi 全部風險的機構參與者。

For investors navigating this landscape, sustainable DeFi participation requires distinguishing between genuinely innovative yield sources and unsustainable mechanisms designed primarily to attract capital. The growing array of analytical tools, risk frameworks, and historical data makes this distinction increasingly possible for sophisticated participants.

對於投資者而言,若要在這個局面下可持續參與 DeFi,就必須區分何者屬於實質創新的收益來源,何者僅為吸資的不可持續機制。分析工具、風險架構和歷史數據日益豐富,亦讓這道分野愈來愈明確。

The broader significance extends beyond individual investors. DeFi's ability to generate sustainably higher yields than traditional finance - even if more modest than early returns - represents a potentially transformative development in global capital markets. By creating more efficient financial infrastructure and disintermediating rent-seeking entities, DeFi could ultimately raise the baseline return on capital throughout the economy, benefiting savers and productive enterprises alike.

這帶來的意義已不僅局限於個人投資者。即便收益幅度趨於較早期為低,DeFi 若能穩定產生高於傳統金融的報酬,仍可能在全球資本市場帶來顛覆性變革。其經由建構更高效的金融基礎設施並消除尋租中介,最終有望拉高整體經濟的資本回報底線,讓儲蓄者與生產性企業雙雙受益。

Up to date, one conclusion seems increasingly clear: while DeFi's triple-digit APYs were largely a temporary phenomenon of its bootstrapping phase, a significant portion of its yield advantage appears fundamentally sustainable - not because of speculative tokenomics, but because blockchain technology enables genuinely more efficient financial systems. The future likely holds neither the extraordinary returns of DeFi's early days nor complete convergence with traditional finance, but rather a new equilibrium that permanently raises the bar for what investors can expect from their capital.

截至目前,有一項結論正日益明朗:DeFi 早期三位數年化收益率,多數只是引導起步時的過渡現象,而現今絕大部分的收益優勢已呈可持續性——並非源於投機式代幣經濟,而是來自區塊鏈技術讓金融系統更有效率。未來不太可能重現 DeFi 幕起之初的驚人暴利,但也不會與傳統金融完全趨同,而是持續在一個新的均衡點上,永久提升投資人對資本回報的期望水準。